(Graphic courtesy Omdia)

Report: Building owners not fully leveraging data from smart solutions

7.22.20 - SIW - Visit SIW for more info

Omdia survey finds that a majority of end users are retaining data generated by their facilities but that many still do not analyze it for patterns

According to a new report Omdia, building owners and operators are not fully realizing the value of the data that being collected by the smart systems and products they currently have installed.

In fact, the market research firm’s new Smart Buildings Survey found that while 77% of end users keep the data generated by their facilities, 42% do not analyze building data to identify variations and patterns that could be used to improve building operation and management. Despite this, the survey, which included responses from 248 smart building technology end users, also found that respondents were willing to invest in smart-building technologies and are event ambitious about the goals they want to achieve with these solutions.

Omdia estimates the global market for building management system (BMS) platforms in terms of supplier revenues was worth $2.5 billion in 2019, while the market for connected equipment reached $12.3 billion the same year. With a large proportion of users still yet to tap the potential of their data, this market has strong growth potential.

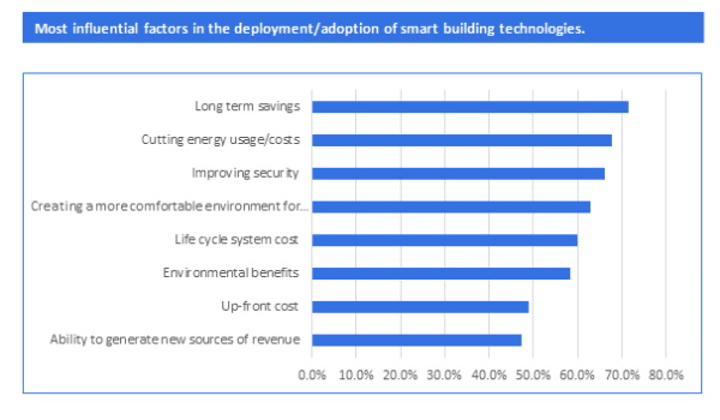

In analyzing why end-users adopt smart building technologies, the primary reason is clearly to manage costs. Long term savings and cutting energy usage/costs were positioned as the two main influencers for end users when it comes to deploying smart-building technologies in their facilities.

“Users’ focus on cost management is not surprising given that this area has long been perceived as the key driver behind the investment in smart-building technologies,” said Thomas Barquin, senior analyst for smart buildings at Omdia. “Creating a more comfortable environment for customer/employee retention is ranked next. This ties in with other Omdia research that suggests an increasingly human-centric focus is becoming a prevalent business driver for the industry, influencing investment decisions and smart-building strategies in some verticals such as office buildings and hotels.”

However, Omdia noted that the smart building industry still faces several challenges, such as the prevalence of legacy systems in existing non-residential buildings, which is ranked as the biggest challenge for end users when implementing IoT and/or smart building technologies.

“Existing buildings often depend upon legacy systems to store and process data, slowing the transition toward smarter buildings,” Barquin said. “This ties in with the third-biggest challenge named in the survey, which involves issues with the interoperability of software solutions. For a long time, the challenges that prevented the rapid growth of the integration of domains through BMS platforms concerned the lack of sufficient connectivity and interoperability between devices and equipment within the building system.”

However, according to Omdia, the market for most connected equipment domains has shifted away from favoring proprietary protocols and toward open protocols over the past decade, as tracked by the research firm in multiple industries.

Even considering these challenges, smart building end-users are willing to invest further in smart building products and are looking for solutions to offer both flexibility and usability. For example, end-users are mostly in favor of using BMS platforms (74%) and equipment as-a-service solutions (69%) as this business model offers end-users access to smart building technologies at a reduced up-front cost. As BMS platform and equipment providers attempt to introduce more software, remote services, and smart equipment to the market, new business models such as software and domain as-a-service brings flexibility to both vendors and end-users.

Finally, artificial intelligence (AI) is gradually starting to play a role in smart buildings and has an immense potential to make smart buildings truly smart and adaptive, rather than just automated. According to Omdia, the market for AI analytics in smart buildings was estimated to be worth $257.5 million in 2019, which represented 10.2 percent of global BMS platform market revenues.

“There is both belief in AI and investment in its solutions for smart buildings, with 87 percent of survey respondents saying they believe AI will become a necessary element of smart-building management,” Barquin said. “AI is considered the natural way forward and should help increase operational efficiency and effectiveness as these solutions continue to develop.”