3.15.21 – Leader Call — By Gordon Fellows - Special to the Leader-Call

Last week, the U.S. Small Business Administration and the U.S. Treasury announced another round of changes to the Paycheck Protection Program that may affect thousands of self-employed Mississippians.

Since the global health crisis began over a year ago, Mississippi banks have been working to support local businesses and consumers who have experienced numerous economic challenges. When Congress passed the CARES Act, which included the Paycheck Protection Program, banks were placed squarely in the middle of the economic response to the unemployment problems created by COVID-19.

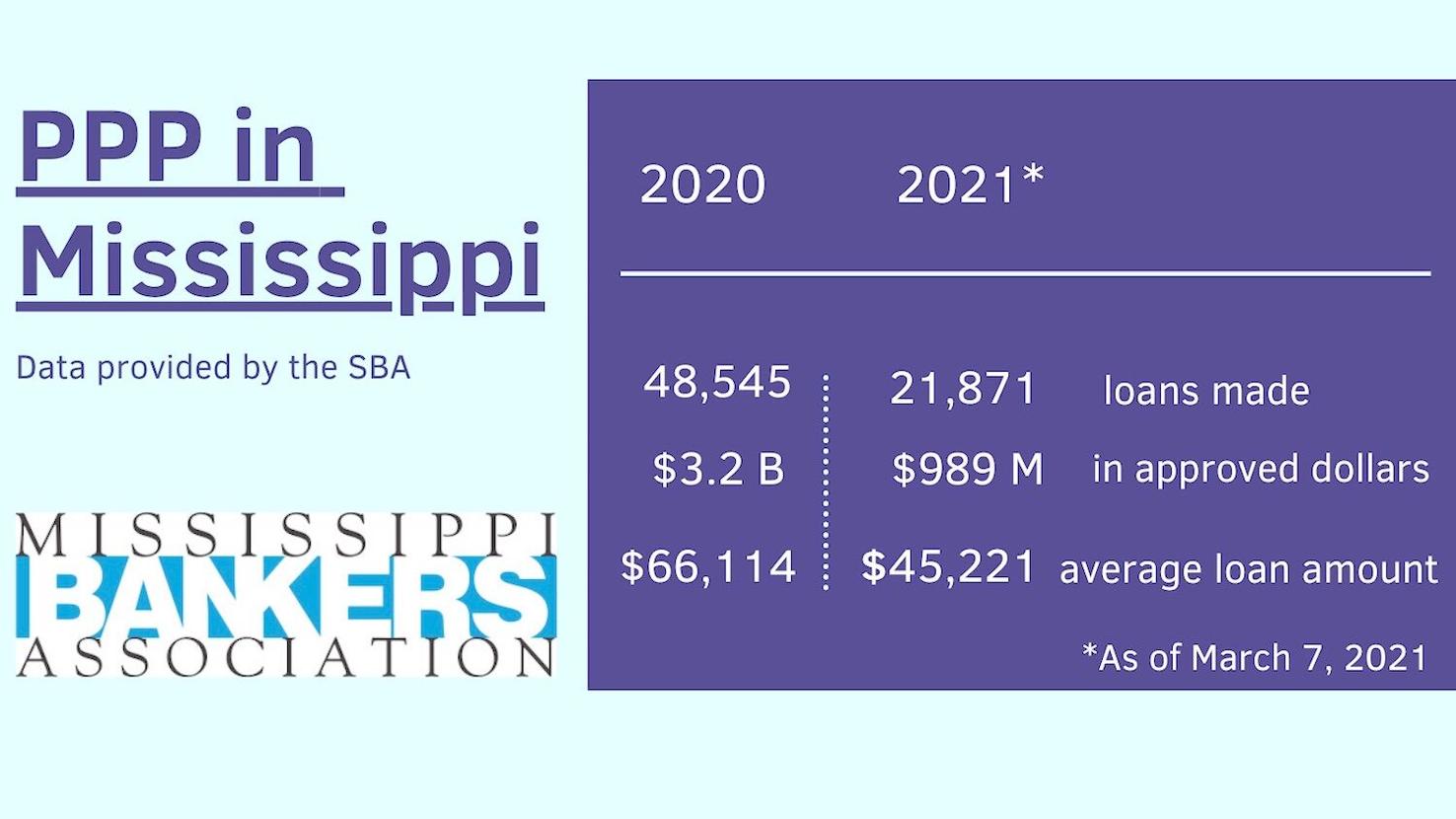

As the state’s unemployment rate climbed to north of 16 percent last spring, Mississippi banks began working through myriad program challenges to start originating these important loans. When the program closed in 2020, several year-end reviews found that Mississippi was one of the most efficient states in the country is executing this important program. In 2020, Mississippi lenders provided more than $3.2 billion in payroll support to employers.

PPP has been bumpy. The SBA and U.S. Treasury had the unenviable task of rapidly building out the rules and technology systems required to implement this important relief program in the middle of an unprecedented crisis, and this was not an easy process. Change has been one of the defining characteristics of PPP since its creation last spring. There have been countless rules changes, form changes, guidance changes and systems changes, all well-intended to help make this critical unemployment-avoidance program more efficient. But nearly each of these changes has been imperfect, and most have created additional challenges for banks, accountants and borrowers to work through.

Last week, the Biden Administration announced another new change that will be important for the thousands of Mississippians who are self-employed and file a 1099 Schedule C to report their business income. The formula used to calculate a borrower’s potential maximum loan amount was adjusted to allow the borrower to elect to use gross revenue as the basis of the calculation instead of net profit. As with most other PPP changes, there’s good news and there is bad news.

Throughout the history of PPP, the reliance on net profit instead of gross revenue has put 1099 Schedule C filers in a difficult situation — while many of these businesses technically qualify for a PPP loan, the maximum amount was often too small to make a difference or justify the borrower spending required time on loan or forgiveness applications. Mississippi banks have always been willing to make small PPP loans to sole proprietors (according to publicly available data, the smallest bank loan made in 2020 to a sole proprietor in Mississippi was $137), but many self-employed borrowers have not participated in the program, and those who have participated received very a small amount of funds relative to other types of small businesses.

So here is the good news: This change means many Schedule C filers such as truck drivers, realtors, charter-boat captains, mom-and-pop retail and restaurant owners and many others may now qualify for substantially larger sums of relief than what was available under the old formula.

And here is the bad news: This change does not have a retroactive function. That means that any Schedule C filer who already received both a first- and second-draw PPP loan using the old formula will not be able to amend his or her existing loan to take advantage of this change. Businesses should know that banks began actively advocating for a retroactive feature to be included in this change when the White House announced in early March that this change was imminent. It is extremely unfortunate that a retroactive option was not considered in the announced rule change.

So, if you are a Schedule C filer and have not yet discussed this new change to PPP with your CPA or your banker, we encourage you to do so soon. Unless Congress acts to again extend the program, PPP will expire at the end of March. Whatever happens with the future of the program, Mississippi banks are committed to working with small businesses all over our state. And there is still plenty of time to benefit from this change if you qualify, but don’t wait too long to contact your lender.

•

Gordon Fellows is president and CEO of the Mississippi Bankers Association.